What they built, what they promised, who paid the price, and whether the math actually works

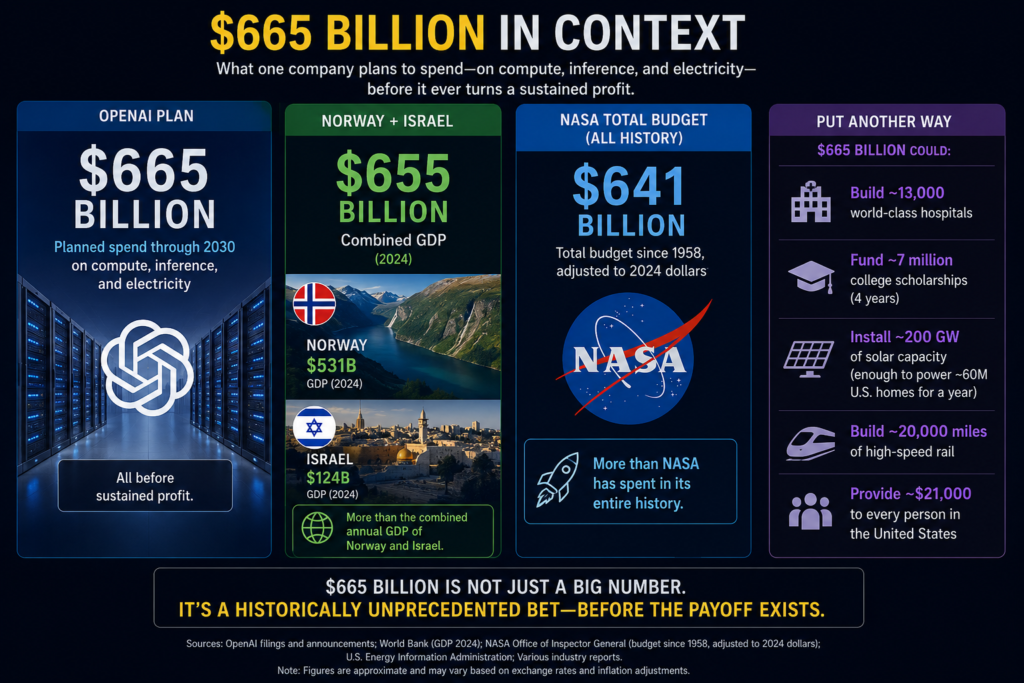

There is a number that should sit on every reader’s whiteboard before going further: $665 billion.

That is what OpenAI now expects to burn through cash by 2030, according to internal documents reviewed by The Information and CNBC in February 2026 — roughly $111 billion more than its earlier projection. The same documents put cash burn at $25 billion in 2026 and $57 billion in 2027 alone. The company does not expect to be cash-flow positive until 2030.

For context: $665 billion is more than the combined annual GDP of Norway and Israel. It is more than NASA has spent in its entire history. It is what one company plans to spend, on compute and inference and electricity, before it ever turns a sustained profit.

This article is about that number, and the two other numbers like it that anchor the modern AI industry. It is about what OpenAI, Anthropic, and the entity formerly known as xAI — now SpaceXAI — have actually built. It is about how fast they grew, what their leaders promised on stage and in print, and how those promises became the cultural permission slip for a wave of layoffs that has now affected hundreds of thousands of workers. And it is about whether the underlying economics — the cost of the chips, the cost of the electricity, the cost of the talent, the cost of the inference — can possibly close the gap before the money runs out.

The honest answer, today, is that nobody knows. But the people inside these companies are betting their lives, and your job, that it will.

I. What They Built

OpenAI

OpenAI began in 2015 as a nonprofit research lab and pivoted to a “capped-profit” hybrid in 2019. Its inflection point was November 30, 2022, when ChatGPT launched and acquired 100 million users in two months — the fastest consumer product adoption in history at the time. Three and a half years later, ChatGPT has roughly 800–900 million weekly active users and generates approximately 2.5 billion queries per day.

The product surface has expanded relentlessly: GPT-5 (the flagship reasoning model), Sora (video generation), Operator and ChatGPT Agent (browsing and task automation), Codex (developer tooling), a custom GPT marketplace, an enterprise tier, a Pentagon contract permitting use “for all lawful purposes” within DoD policy, and — most consequentially — Stargate, a data-center buildout co-financed with SoftBank, Oracle, and Crusoe, with announced commitments approaching $500 billion across roughly 10 gigawatts of capacity.

By revenue, OpenAI went from approximately $200 million in 2022 to $13.1 billion in 2025, hit a $20 billion annualized run-rate by year-end 2025, and reached roughly $24 billion (about $2 billion per month) by April 2026. In the same month, the company closed a $122 billion funding round at an $852 billion valuation, co-led by SoftBank with Andreessen Horowitz, D.E. Shaw, MPX, TPG, and existing investors. Microsoft, under a renegotiated October 2025 partnership, holds a 27% diluted stake and receives 20% of OpenAI’s revenue through 2032.

Anthropic

Anthropic was founded in 2021 by Dario and Daniela Amodei and a small group of former OpenAI researchers who left over disagreements on safety and governance. From the beginning, Anthropic positioned itself as the enterprise-and-safety alternative — Claude was launched in March 2023 with a 100,000-token context window when ChatGPT was capped at 4,000–32,000 — and the bet on B2B paid off.

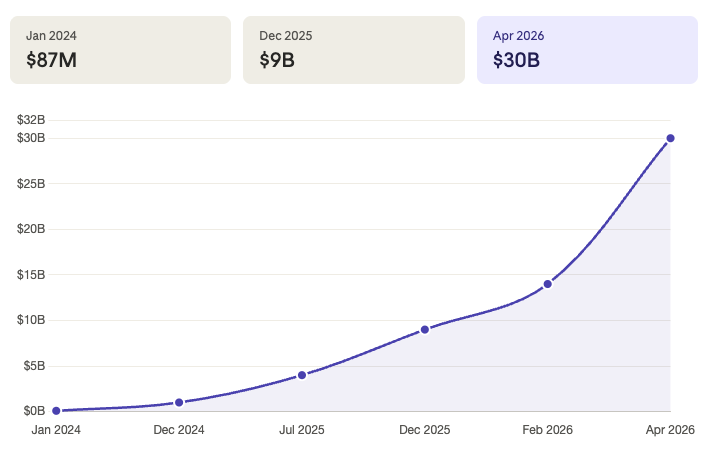

The growth curve is, honestly, hard to make sense of in traditional software terms. Anthropic was at roughly $87 million in run-rate in January 2024. $1 billion by December 2024. $4 billion by mid-2025. $9 billion by end of 2025. $14 billion by mid-February 2026. $30 billion by April 2026.

Salesforce took roughly twenty years to reach $30 billion in annual revenue. Anthropic did it in under three years from a standing start. Around 80% of that revenue is enterprise, a structural advantage that — as we’ll see — gives Anthropic dramatically better unit economics than OpenAI. Claude Code alone, launched in May 2025, hit a $2.5 billion run-rate by February 2026, doubling weekly active users since the start of the year.

The funding has matched the curve: $13 billion at a $183 billion valuation in September 2025, $30 billion at a $380 billion valuation in February 2026 (led by GIC and Coatue), and as of late April 2026, TechCrunch reported Anthropic is in talks for a further $50 billion round at a valuation of $850–900 billion. Eight of the Fortune 10 are now Claude customers. Over 500 companies spend more than $1 million annually on Claude.

SpaceXAI (formerly xAI)

xAI was Elon Musk’s belated entry into the frontier-model race, founded in March 2023 with eleven researchers after Musk’s break with OpenAI. Its flagship product is Grok, an assistant integrated tightly into X (formerly Twitter, which xAI acquired in an all-stock deal in March 2025). The infrastructure centerpiece is Colossus, a Memphis supercomputer that grew from 100,000 GPUs at the end of 2024 to over 555,000 GPUs by early 2026 — at an estimated $18 billion hardware cost — with a stated 2-gigawatt power target.

The trajectory has been turbulent. Grok grew its US chatbot market share roughly ninefold during 2025, peaking as the world’s second-most-used AI assistant. By April 2026 it had fallen to fifth, overtaken by Claude, Gemini, and DeepSeek. Daily active users on Grok mobile dropped from 13.9 million in March 2026 to 12.2 million in April. In the same window, Claude’s daily actives jumped from 16 million to 23 million.

In February 2026, SpaceX absorbed xAI in an all-stock transaction valuing xAI at $250 billion within a $1.25 trillion combined entity — described as the largest private corporate merger in history. By May 2026, Musk announced xAI would cease to exist as a separate company, becoming a sub-brand called SpaceXAI within SpaceX. All eleven original co-founders had departed by March 2026; the CFO left in April; SpaceX’s Starlink VP became xAI’s president. Days before the dissolution, SpaceX agreed to lease 300 megawatts of Colossus 1 capacity — equivalent to about 220,000 GPUs — to Anthropic. Musk himself had publicly called xAI “inferior” to its rivals.

xAI raised over $42 billion across all rounds, and reportedly burned $7.8 billion in the first nine months of 2025 alone — about $28 million per day. Q3 2025 net loss was $1.46 billion, up from $1 billion in Q1.

II. The Speed of It

It is worth pausing on how fast all of this happened, because the speed itself is part of the story. ChatGPT did not exist four years ago. Claude did not exist five years ago. Colossus 1 did not exist three years ago. By the time you read this, the combined enterprise value of these three companies and their parent entities is approaching $3 trillion in private market valuations — more than the GDP of France.

For comparison: it took Google seven years to reach $12 billion in annual revenue. It took Facebook six years. OpenAI did it in under three. Anthropic compressed that further. Meritech’s Alex Clayton, who has reviewed the IPO trajectories of more than 200 public software companies, said publicly in 2025 that he had never seen growth rates like Anthropic’s. The trajectory has only accelerated since.

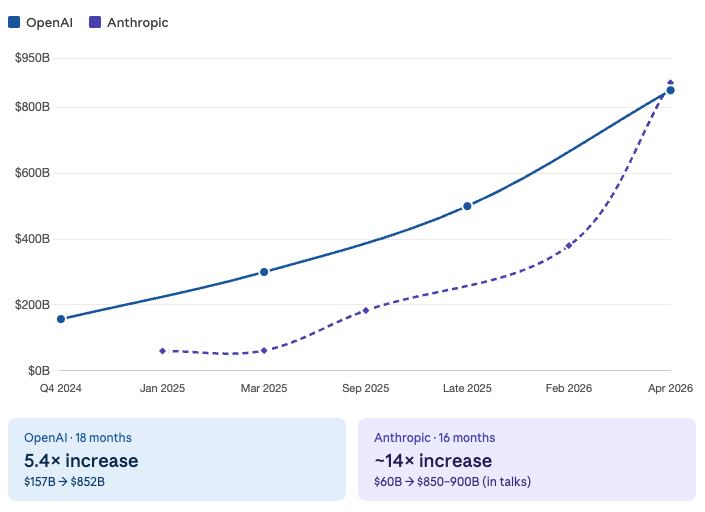

This speed was funded almost entirely by private capital, and the capital itself moved at a pace that broke historical precedent. Anthropic’s valuation moved from roughly $60 billion in January 2025 to $61.5 billion in March, to $183 billion in September, to $380 billion in February 2026 — and is now being negotiated at $850–900 billion. That is a roughly 14x increase in 16 months for a company whose underlying revenue, while spectacular, still leaves it valued at 27 times annualized revenue at the February mark.

OpenAI’s valuation went from approximately $157 billion in late 2024 to $300 billion in March 2025 to $500 billion in late 2025 to $852 billion in April 2026.

III. What the Leaders Said

The narrative that justified those valuations did not come from spreadsheets. It came from what the founders said in interviews, on stages, in shareholder letters, and on podcasts — a steady, escalating drumbeat of claims about what AI was about to do to human work.

Dario Amodei has been the most explicit. At Davos in January 2026, he told the audience that AI models would replace the work of all software developers within a year and reach “Nobel-level” scientific research in multiple fields within two. In a widely cited interview, he predicted 50% of entry-level white-collar jobs could disappear within five years, with unemployment potentially climbing to 20%. He has described his vision as “a country of geniuses in a datacenter” by 2026. He told Fortune that a twelve-month delay in AI progress would make him personally bankrupt.

Sam Altman has played a more elliptical game. He declared in late 2024 that we were beginning to slip past human-level AGI toward “superintelligence.” He has projected $100 billion in annual revenue for OpenAI by 2027 and $200–280 billion by 2030. He also, in August 2025, told reporters: “Are we in a phase where investors as a whole are overexcited about AI? My opinion is yes.” And at the India AI Impact Summit in early 2026, he conceded what had become impossible to deny: “There’s some AI washing where people are blaming AI for layoffs that they would otherwise do.”

Elon Musk has predicted AGI by 2025, then by 2026, while telling staff that xAI would “catch up and close the gap” by the end of 2026. By May 2026 — months before that deadline — he had folded the company into SpaceX and admitted it was inferior.

Mustafa Suleyman, now at Microsoft AI, predicted “human-level performance” on most professional tasks within 12–18 months in a February 2026 interview. Demis Hassabis at Google DeepMind has been more measured, putting genuine AGI on a multi-year horizon and noting “maybe we need one or two more breakthroughs before we’ll get to AGI.” Geoff Hinton, the Nobel laureate, has revised his estimate repeatedly toward the near term while expressing deep uncertainty.

These claims were not academic. They were spoken into a financial system primed to act on them, and into a labor market whose CFOs and CEOs were looking for a new vocabulary to justify decisions they had already made or wanted to make.

IV. The Sentiment That Cost Millions Their Jobs

By the spring of 2026, AI had become the single most powerful explanatory frame in corporate communications. Whether or not the technology was actually capable of doing the work, the narrative that it was capable of doing the work had become a corporate asset — a way to deliver bad news while signaling to shareholders that you were forward-leaning, modern, and disciplined.

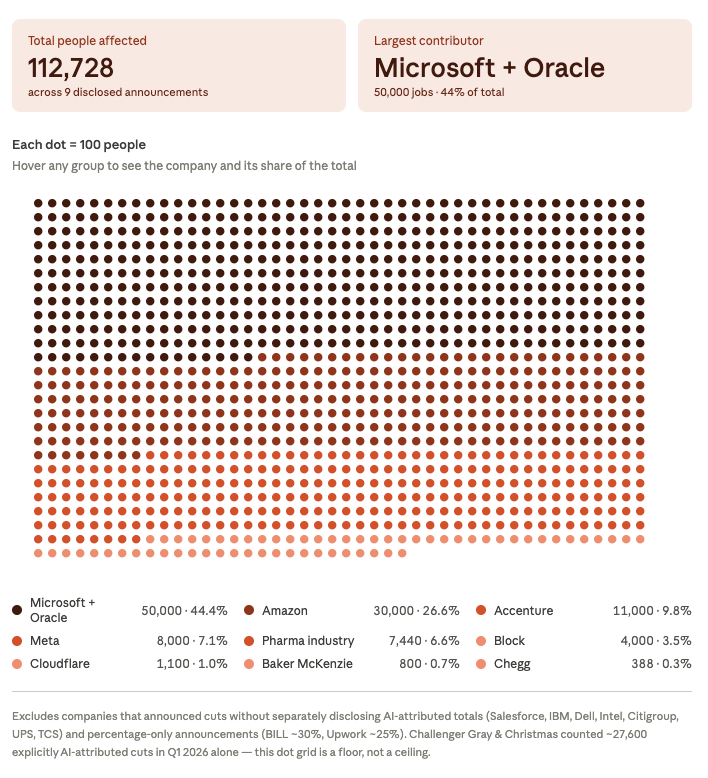

The numbers are stark. In 2025, more than 100,000 employees were impacted by layoffs that companies explicitly attributed, in whole or part, to AI. In just the first quarter of 2026, the tech industry alone shed nearly 80,000 jobs, with up to half of those positions cited as AI-driven. Through April 2026, AI was named as a factor in roughly 27,600 layoffs — about 13% of all announced cuts, up from 5% in 2025. By mid-2026, Challenger reports placed the “AI-attributed” cumulative figure across industries above 70,000 workers in 2026 alone.

A non-exhaustive list of what was announced:

- Amazon: ~30,000 corporate jobs across late 2025 and January 2026, with SVP Beth Galetti citing AI as one reason for operating with fewer people.

- Accenture: ~11,000 in December 2025, tied to “how work is changing inside the firm.”

- Microsoft, Oracle: more than 50,000 combined since January 2026.

- Meta: 8,000 roles eliminated starting May 2026.

- Block: ~4,000 — nearly halving headcount — with Jack Dorsey writing that “intelligence tools have changed what it means to build and run a company.”

- Salesforce, IBM, Dell, Intel, Citigroup, UPS, TCS: each in five-figure cuts, often paired with AI-themed restructuring language.

- Chegg: 45% of staff, with the cause openly attributed to students using ChatGPT.

- Cloudflare: 1,100 in May 2026, citing a 600% rise in internal AI usage.

- BILL: up to 30% of headcount in May 2026.

- Upwork: roughly 25% of workforce in May 2026.

- Baker McKenzie: 600–1,000 staff, primarily research, marketing, and secretarial roles.

- Pharmaceutical industry: 7,440 announced cuts year-to-date by May 2026 — a 500% jump signaling the AI-attribution pattern had escaped tech and was spreading.

The hardest-hit cohort is younger workers. Goldman Sachs flagged Gen Z tech workers as first in line. Unemployment for 22- to 27-year-olds with bachelor’s degrees climbed from a historical norm below the national average to 5.8% in March 2025, and to 6.6% by mid-year — a four-year high. Entry-level white-collar postings on Handshake fell 15% year-over-year while applications-per-job rose 30%. By early 2026, a Cengage Group survey found 75% of employers planned to hire the same number or fewer entry-level workers, up from 69% the year before.

Glassdoor’s tech-sector employee confidence dropped 6.8 points year-over-year — the largest decline of any industry. The median time-to-hire for senior Bay Area engineers stretched from 38 days in Q3 2025 to 67 days in Q1 2026. Tech wages outside specialized AI roles are flat against 2025.

But here is the part that should haunt the narrative: a National Bureau of Economic Research study published in February 2026 found that despite 90% of firms reporting no measurable impact of AI on workplace productivity, executives publicly projected AI would increase productivity by 1.4% and output by 0.8%. The actual operational effect, in other words, has been small. The narrative effect has been enormous.

This is what Sam Altman called AI washing, and what an MIT economist Daron Acemoglu — the 2024 Nobel laureate — has been blunter about: “These models are being hyped up, and we’re investing more than we should… much of what we hear from the industry now is exaggeration.” Marc Andreessen, from a different ideological corner, has said the same thing in different words: the layoffs are about higher interest rates and “a complete loss of discipline” in pandemic-era hiring. The AI explanation is, in many cases, the alibi.

The cost of the alibi is borne by people. Hundreds of thousands of them.

V. The Math: What These Companies Spend, and What They Need

Now we get to the part that nobody who watches CNBC for ninety seconds at a time fully internalizes.

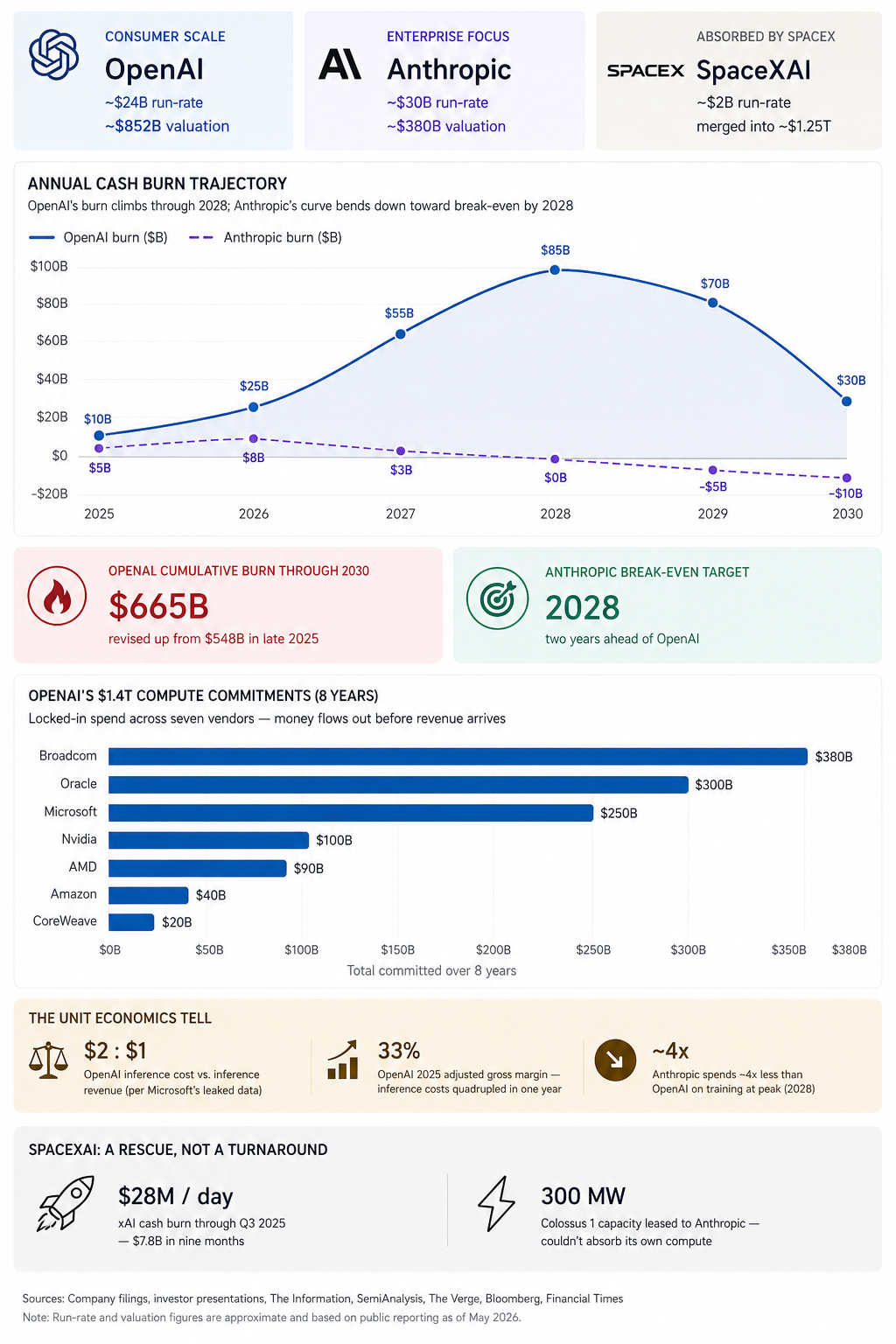

OpenAI

- Revenue 2025: $13.1 billion.

- Net loss, first half of 2025 alone: $13.5 billion.

- Projected 2026 cash burn: $25 billion (revised up from $17 billion).

- Projected 2027 cash burn: $57 billion.

- Cumulative cash burn through 2030: $665 billion (revised up from $554 billion in late 2025).

- Adjusted gross margin 2025: 33%, down from previous estimates as inference costs quadrupled in a single year.

- Compute commitments: $1.4 trillion across eight years to companies including Broadcom ($350B), Oracle ($300B), Microsoft ($250B), Nvidia ($100B), AMD ($90B), Amazon ($38B), and CoreWeave ($22B).

- Cash on hand: $40 billion (as of February 2026).

- Active fundraising target: more than $100 billion.

- HSBC analysts’ estimate of additional capital required to deliver on growth plans: $207 billion.

- Microsoft’s leaked data: OpenAI burns roughly $2 in inference cost for every $1 of inference revenue.

OpenAI is making, as one Substack analyst put it, “money hand over fist” — and burning more money, faster, than any private company in history. The company expects burn to remain at 57% of revenue in 2026 and 2027, before slowly converging toward profitability around 2030. By 2028, operating losses could equal roughly three-quarters of that year’s revenue. A WSJ-cited internal projection puts OpenAI’s 2028 losses at $85 billion against $121 billion in compute spending in that single year.

Anthropic

- Revenue 2025 (year-end run-rate): ~$9 billion.

- Revenue April 2026 (run-rate): ~$30 billion.

- Projected burn rate as % of revenue: ~33% in 2026, dropping to ~9% in 2027.

- Projected break-even: 2028.

- Total capital raised: over $18 billion as of February 2026; potentially $50 billion more in the negotiating round.

- Training cost peak (2028): ~$30 billion — roughly 4x less than OpenAI’s peak.

The structural difference matters. Anthropic chose enterprise; OpenAI chose consumer scale. Enterprise customers pay more per query, churn less, and don’t expect a free tier subsidized by the rest of the business. The result is that Anthropic, despite having raised dramatically less and built smaller infrastructure, is on track to stop burning cash two years before OpenAI — while running a business of comparable scale.

This is the “narrative violation” that Anthropic’s recent confidential filings revealed: the company that just passed OpenAI on revenue run-rate is doing it while spending a fraction of what OpenAI spends on training.

SpaceXAI / xAI

- Estimated 2025 revenue (Grok): ~$350 million.

- Estimated 2026 revenue: ~$2 billion.

- Burn 2025 (first nine months): $7.8 billion — ~$28 million per day.

- Q3 2025 net loss: $1.46 billion.

- Stated infrastructure spend rate: ~$1 billion per month.

- Total funding raised pre-merger: over $42 billion.

- Combined SpaceX entity valuation: $1.25 trillion.

xAI’s economics were the worst of the three by every measure that matters — revenue, market share trajectory, and unit cost of compute. The merger into SpaceX is, in financial terms, a rescue: by absorbing xAI, Musk has both shielded its balance sheet from independent investor scrutiny and given SpaceX the opportunity to position any future IPO as an “AI infrastructure” play rather than just a launch-services business. The lease of 300 MW of Colossus 1 capacity to Anthropic — Musk’s bitter rival via Amodei’s OpenAI departure — tells you what you need to know about the standalone economics. xAI could not absorb its own compute. It had to rent it to the competitor.

VI. The Circular Loop

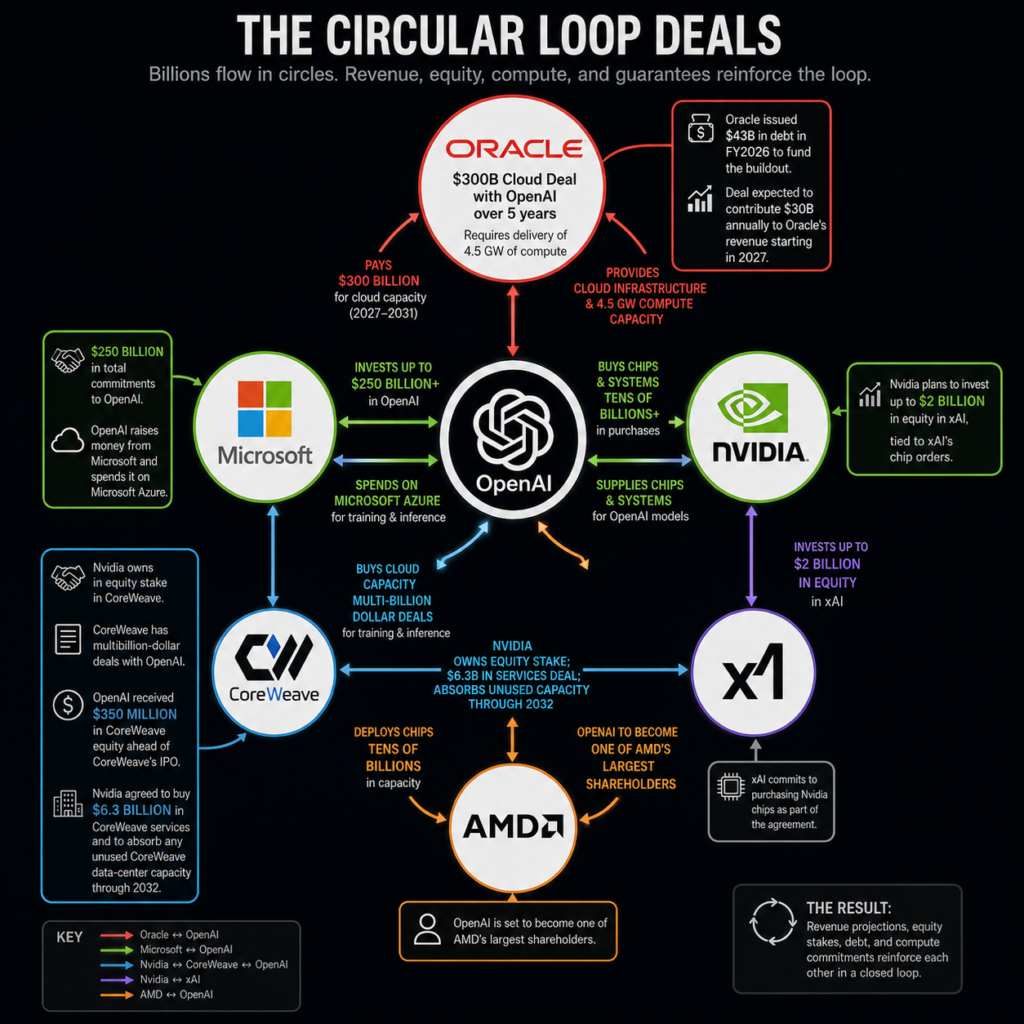

The defining financial feature of this moment is what is now called, in Bloomberg and the Financial Times and increasingly in academic work, circular financing.

The mechanic is straightforward. Nvidia announces it will invest up to $100 billion in OpenAI. OpenAI uses that capital to build data centers. The data centers are filled with Nvidia chips. Cash flows out of Nvidia, travels through OpenAI’s balance sheet, and returns to Nvidia as revenue. Both companies report growth. Investors see a flywheel.

The same pattern, at varying scales, runs through:

- Oracle ↔ OpenAI: a $300 billion, five-year cloud deal, requiring Oracle to deliver 4.5 gigawatts of compute. Oracle issued $43 billion in debt in fiscal 2026 to fund the buildout. The deal is expected to contribute $30 billion annually to Oracle’s revenue starting in 2027.

- Microsoft ↔ OpenAI: $250 billion in commitments; OpenAI raises money from Microsoft and spends it on Microsoft Azure.

- Nvidia ↔ CoreWeave ↔ OpenAI: Nvidia owns part of CoreWeave; CoreWeave has multibillion-dollar deals with OpenAI; OpenAI received $350 million in CoreWeave equity ahead of CoreWeave’s IPO; Nvidia agreed to buy $6.3 billion in CoreWeave services and to absorb any unused CoreWeave data-center capacity through 2032.

- Nvidia ↔ xAI: Nvidia plans to invest up to $2 billion in equity in xAI, tied to xAI’s chip orders.

- AMD ↔ OpenAI: tens of billions in chip deployments; OpenAI is set to become one of AMD’s largest shareholders.

Janus Henderson and other defenders call this a “virtuous circle” — a way to lock in supply during a chip shortage. Critics, including INSEAD’s faculty, Harvard Kennedy School’s Paulo Carvao, and MIT’s Acemoglu, point to a precedent: the late-1990s telecoms used vendor financing — equipment makers loaned money to carriers to keep buying their gear — and reported the resulting orders as revenue. When demand projections finally fell short, the carriers couldn’t pay, the equipment makers wrote down billions, and capacity sat unused for years. Qwest and Global Crossing both ended up in U.S. Congressional investigations over similar “capacity swaps.”

Michael Burry — yes, that one — wrote on X in late 2025: “True end demand is ridiculously small. Almost all customers are funded by their dealers,” and followed up with “OpenAI is the linchpin here. Can anyone name their auditor?” Peter Thiel sold his entire roughly $100 million Nvidia stake in November 2025. SoftBank dumped a nearly $6 billion Nvidia position around the same time.

Morgan Stanley estimates global data-center spending between 2025 and 2028 will reach $3 trillion. Roughly half of that is being financed by private credit. Big Tech’s combined 2026 AI capex is on track to exceed $660 billion. Alphabet’s announcement that it would spend $175–185 billion in 2026 — roughly double 2025 — triggered an immediate sell-off. The market’s reaction to that capex disclosure, in the words of one INSEAD analysis, was “sharp repricing rather than applause.” Investors are no longer applauding the scale. They are policing the conversion path.

VII. What End-of-2027 Looks Like

This is the question the user asked, and it is the question the industry is most reluctant to answer cleanly. Here is what the public projections imply.

By end of 2027, OpenAI alone needs to have raised, drawn down, or otherwise financed approximately $82 billion in cumulative cash burn for 2026 and 2027 combined ($25B + $57B). That is on top of existing commitments. The April 2026 raise of $122 billion — combined with the $40 billion cash position, the renegotiated Microsoft revenue share, the Stargate vehicle, and incoming sovereign wealth from Gulf funds — gets it through 2027 mathematically, if revenue tracks the company’s bullish projections (roughly $50–70 billion run-rate by year-end 2027) and if training and inference costs do not rise faster than expected. Both of those conditions have already been broken once: inference costs quadrupled in 2025, and the burn projection itself was revised upward by $111 billion in February 2026.

If revenue undershoots — if ChatGPT subscription growth saturates, if enterprise adoption stalls, if a competitor like Anthropic, DeepSeek, or Gemini compresses pricing further — OpenAI will need another raise of $50–100 billion sometime in 2027. The HSBC estimate of $207 billion in additional capital required suggests this is closer to the base case than the worst case. Asia Times, citing analysts, has gone further and floated bankruptcy as a possibility “as early as 2027” if external financing falters. That reporting represents the bear case, not consensus, but the consensus path itself depends on near-perfect execution and continued investor appetite.

Anthropic’s end-of-2027 picture is the most defensible. With a projected burn declining to ~9% of revenue in 2027 and break-even targeted for 2028, Anthropic likely needs only one more large round — the $50 billion currently being negotiated at $850–900 billion — to bridge to profitability. If enterprise demand holds and Claude Code continues its trajectory (it has already roughly tripled in months), Anthropic can plausibly be self-funding by the end of 2027 or shortly thereafter.

SpaceXAI’s end-of-2027 picture is now SpaceX’s problem. As an absorbed sub-brand within a $1.25 trillion combined entity targeting a Nasdaq IPO in mid-2026 at a potential $1.75 trillion valuation, the AI division’s standalone economics matter less than the optics of having an AI story to tell public investors. The $300 MW lease to Anthropic, the departure of every co-founder, and the dissolution of the brand all suggest the AI bet has been quietly wound down to a supporting role. Expect the AI line item in SpaceX’s S-1 filing to be marketed as forward-looking infrastructure rather than near-term revenue.

The systemic question is what happens if any one of these companies stumbles. The circular-financing graph means that a serious revenue miss at OpenAI threatens Oracle’s debt service, which threatens its $300B contract execution, which threatens CoreWeave’s order book, which threatens Nvidia’s data-center segment, which threatens the equity values inside half the public market’s index funds. Credit default swap spreads on Oracle have nearly doubled since September 2025. The market is, quietly, beginning to price the tail risk.

VIII. What This Article Is Actually About

It is tempting, after walking through these numbers, to conclude that the AI boom is a fraud, or a bubble, or a cynical wealth transfer. Some of that conclusion is defensible. A great deal of it is not. The technology is genuinely useful. Anthropic’s revenue is real. Enterprise customers are paying because Claude and ChatGPT are saving them measurable amounts of work. Coding has been transformed. Drug-discovery pipelines have been compressed. The fact that NBER finds 90% of firms reporting no productivity impact does not negate the 10% where the impact is real and growing.

But the framing of the AI moment — the framing that has been used to justify hundreds of thousands of layoffs, trillions in capital reallocation, and the gutting of entry-level career pipelines for an entire generation — is not the same thing as the technology itself. The framing was constructed by a small group of CEOs whose personal financial outcomes depend, with extraordinary precision, on the framing being believed.

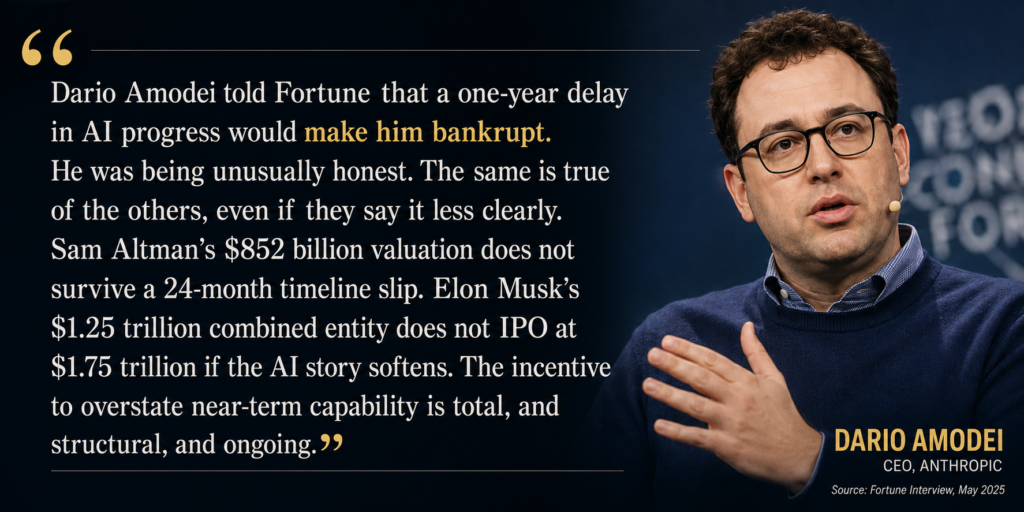

Dario Amodei told Fortune that a one-year delay in AI progress would make him bankrupt. He was being unusually honest. The same is true of the others, even if they say it less clearly. Sam Altman’s $852 billion valuation does not survive a 24-month timeline slip. Elon Musk’s $1.25 trillion combined entity does not IPO at $1.75 trillion if the AI story softens. The incentive to overstate near-term capability is total, and structural, and ongoing.

Meanwhile, the people who lost their jobs in the name of AI productivity gains — the 4,000 at Block, the 11,000 at Accenture, the 30,000 at Amazon, the half-cohort of new graduates who will never get the entry-level role that would have launched their career — those people are bearing the cost of a narrative whose authors have publicly admitted, in moments of candor, that the narrative is at least partly inflated.

The end-of-2027 question, then, is not really will OpenAI go bankrupt. It is something harder and more uncomfortable.

It is: what do we owe each other, when a small number of people make extraordinary claims about a technology that is partly real and partly story, and the rest of the economy reorganizes itself around those claims as if they were fully real?

If the technology delivers what the founders promised, OpenAI’s $665 billion looks cheap, Anthropic’s $900 billion valuation looks like a bargain, and the layoffs were a painful but necessary reorganization toward higher productivity. If it doesn’t — if the curves bend, if the inference costs don’t fall, if the next training run delivers a 10% improvement instead of a 100% improvement — then a generation of young workers paid the cost for a bet that the people who placed it knew was riskier than they let on.

We will know which one it is, with reasonable certainty, by the end of 2027.

Until then, the most useful posture is neither belief nor cynicism. It is attention. Watch the burn rates. Watch the inference costs. Watch the credit default swaps on Oracle. Watch which CEOs quietly soften their AGI timelines when they think nobody is listening. Watch whether the laid-off worker at Accenture or the graduate from a state college who can’t find a junior analyst job ever shows up in the productivity statistics that the founders promised.

Watch the math.

The math is the only part of this story that cannot be marketed.

Sources:

Figures and quotations are drawn from the following reports, published between September 2025 and May 2026.

Company financials and valuations

- Sacra, OpenAI revenue, valuation & funding — https://sacra.com/c/openai/

- Sacra, Anthropic revenue, valuation & funding — https://sacra.com/c/anthropic/

- Sacra, xAI revenue, valuation & funding — https://sacra.com/c/xai/

- Anthropic, Anthropic raises $30 billion in Series G funding at $380 billion post-money valuation (Feb 12, 2026) — https://www.anthropic.com/news/anthropic-raises-30-billion-series-g-funding-380-billion-post-money-valuation

- CNBC, Anthropic closes $30 billion funding round at $380 billion valuation (Feb 12, 2026) — https://www.cnbc.com/2026/02/12/anthropic-closes-30-billion-funding-round-at-380-billion-valuation.html

- TechCrunch, Sources: Anthropic could raise a new $50B round at a valuation of $900B (Apr 29, 2026) — https://techcrunch.com/2026/04/29/sources-anthropic-could-raise-a-new-50b-round-at-a-valuation-of-900b/

OpenAI burn rate, projections, and IPO documents

- Fortune, OpenAI says it plans to report stunning annual losses through 2028 (Nov 12, 2025) — https://fortune.com/2025/11/12/openai-cash-burn-rate-annual-losses-2028-profitable-2030-financial-documents/

- Yahoo Finance / PC Gamer, OpenAI’s own forecast predicts $14 billion loss in 2026 (Jan 21, 2026) — https://finance.yahoo.com/news/openais-own-forecast-predicts-14-150445813.html

- MLQ.ai (citing The Information and CNBC), OpenAI Revises Projections Upward with $112 Billion Extra Cash Burn by 2030 (Feb 21, 2026) — https://mlq.ai/news/openai-revises-projections-upward-with-112-billion-extra-cash-burn-by-2030/

- Asia Times, OpenAI is burning billions — and an IPO won’t stave off bankruptcy (Apr 2026) — https://asiatimes.com/2026/04/openai-is-burning-billions-and-an-ipo-wont-stave-off-bankruptcy/

- SaaStr, Anthropic Just Passed OpenAI in Revenue. While Spending 4x Less to Train Their Models (Apr 7, 2026) — https://www.saastr.com/anthropic-just-passed-openai-in-revenue-while-spending-4x-less-to-train-their-models/

- Sahi.com, The Burning Billions: Can OpenAI Afford to Win the AI Race (Feb 22, 2026) — https://www.sahi.com/blogs/the-burning-billions-can-open-ai-afford-to-win-the-ai-race

xAI / SpaceX

- TradingKey, SpaceX IPO Approaches: Musk Dissolves xAI into SpaceX (May 7, 2026) — https://www.tradingkey.com/analysis/stocks/us-stocks/261868650-spacex-ipo-xai-anthropic-tradingkey

- Wikipedia, xAI (company) — https://en.wikipedia.org/wiki/XAI_(company)

- SQ Magazine, Grok AI Statistics 2026: Users, Revenue and Growth Data — https://sqmagazine.co.uk/grok-ai-statistics/

- Business of Apps, Grok Revenue and Usage Statistics (2026) (Mar 31, 2026) — https://www.businessofapps.com/data/grok-statistics/

- TSG Invest, xAI Stock: $250B Valuation — https://tsginvest.com/xai/

Layoffs and labor market data

- Challenger, Gray & Christmas, April Job Cuts Rise 38% from March; YTD AI-cited cuts reach 49,135 (May 2026) — https://www.challengergray.com/blog/challenger-report-april-job-cuts-rise-38-from-march-ytd-cuts-down-50/

- CBS News, AI emerges as a top cause of layoffs, accounting for 26% of April’s job cuts (May 2026) — https://www.cbsnews.com/news/ai-layoffs-job-cuts-challenger-report-april-2026/

- Programs.com, List of Companies Announcing AI-Driven Layoffs — https://programs.com/resources/ai-layoffs/

- Tom’s Hardware, Tech industry lays off nearly 80,000 employees in the first quarter of 2026 — https://www.tomshardware.com/tech-industry/tech-industry-lays-off-nearly-80-000-employees-in-the-first-quarter-of-2026-almost-50-percent-of-affected-positions-cut-due-to-ai

- Yahoo Finance, Layoffs Accelerate in May 2026 as Firms Restructure Around AI — https://finance.yahoo.com/sectors/technology/articles/layoffs-accelerate-may-2026-firms-040430218.html

- NewsNation, AI is tied to tech layoffs, but spending — not job replacement — may be the key driver — https://www.newsnationnow.com/business/your-money/tech-layoffs-surge-ai-spending/

- The Dupree Report, Tech Layoffs Hit 85K in 2026 as AI Becomes the Alibi — https://www.thedupreereport.com/33750/

Leadership statements and AGI claims

- Fortune, AI luminaries at Davos clash over how close human-level intelligence really is (Jan 23, 2026) — https://fortune.com/2026/01/23/deepmind-demis-hassabis-anthropic-dario-amodei-yann-lecun-ai-davos/

- Techzine, OpenAI CEO under fire: “The problem is Sam Altman” (Apr 7, 2026) — https://www.techzine.eu/news/analytics/140271/openai-ceo-under-fire-the-problem-is-sam-altman/

- Gizmochina, Will AI Take Your Job? OpenAI CEO Sam Altman Gives a Surprising Answer (May 2, 2026) — https://www.gizmochina.com/2026/05/02/sam-altman-ai-jobs-future/

- Medium / Tim Ventura, AGI Insider Predictions for the Arrival of Human-Level Artificial Intelligence (Feb 2026) — https://medium.com/@timventura/agi-insider-predictions-for-the-arrival-of-human-level-artificial-intelligence-40c1084dbcb3

Bubble, circular financing, and macro analysis

- Bloomberg, AI Circular Deals: How Microsoft, OpenAI and Nvidia Keep Paying Each Other (Mar 11, 2026) — https://www.bloomberg.com/graphics/2026-ai-circular-deals/

- INSEAD Knowledge, Are We in an AI Bubble? (Feb 23, 2026) — https://knowledge.insead.edu/economics-finance/are-we-ai-bubble

- NPR, Here’s why concerns about an AI bubble are bigger than ever (Nov 23, 2025) — https://www.npr.org/2025/11/23/nx-s1-5615410/ai-bubble-nvidia-openai-revenue-bust-data-centers

- Wikipedia, AI bubble — https://en.wikipedia.org/wiki/AI_bubble

- Investing.com, 2026: Another Year of AI Bubble Not Bursting? (Jan 2, 2026) — https://www.investing.com/analysis/2026-another-year-of-ai-bubble-not-bursting-200672634

- BlockEden, The Great AI Circular Financing Loop (Mar 7, 2026) — https://blockeden.xyz/blog/2026/03/06/ai-circular-financing-loop-vendor-financing/

- Noah Smith, Should we worry about AI’s circular deals? (Oct 22, 2025) — https://www.noahpinion.blog/p/should-we-worry-about-ais-circular

Labor market / Gen Z entry-level data

- AInvest, Gen Z’s Job Crisis: AI Displaces Roles Faster Than Skills Can Adapt (Sep 21, 2025) — https://ainvest.com/news/gen-job-crisis-ai-displaces-roles-faster-skills-adapt-2509

- Newser, Gen Z Job-Seekers Have Big New Problem: AI (Jul 15, 2025) — https://www.newser.com/story/371820/gen-z-grads-face-a-big-job-hunting-challenge.html